- Have any questions?

- Office: +1 (650) 345-8510

- Mobile: +1 (650) 576-6916

- norm@traveltechnology.com

Farelogix

February 19, 2013

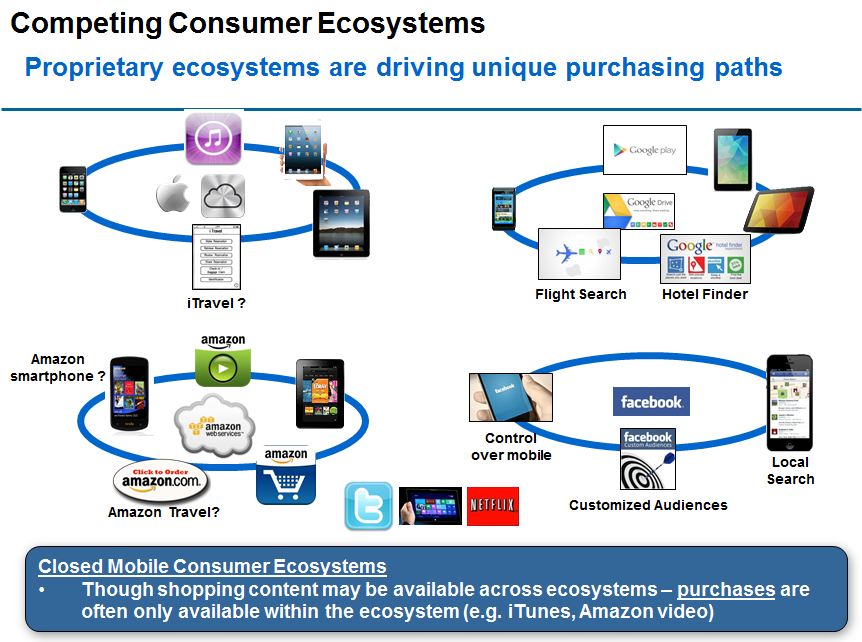

Tweet I was in Miami last week attending the Farelogix Media Day. My presentation entitled The Future of Travel Distribution can viewed via SlideShare. Part of my presentation discussed how competing consumer ecosystems (Apple, Google, Amazon, Facebook) provide unique content and purchasing paths via mobile devices. Over the next five years mobile devices (including tablets) will become the foundation for most travel e-commerce. As a […]